Expressnews

Expressnews

Chennai, July 2026: Knight Frank India, in its latest report India Real Estate: Residential and Office H1 2026 (January–June 2026), highlighted Chennai’s continued resilience across both residential and commercial real estate. The city registered residential sales of 9,198 housing units during H1 2026, recording a 3% YoY increase, while average residential prices appreciated by 5% YoY to INR 7,555 per sq ft, reflecting sustained end-user demand and improving purchasing power.

Residential launches remained largely stable at 9,588 units, underscoring developers’ measured approach to supply despite evolving market dynamics. Demand continued to shift towards the mid and premium housing segments, supported by infrastructure expansion, employment generation across manufacturing and Global Capability Centres (GCCs), and improving connectivity through major infrastructure projects including Chennai Metro Phase II.

On the commercial real estate front, Chennai recorded 3.6 mn sq ft of office leasing during H1 2026. Although transaction volumes moderated by 28% year-on-year due to the exceptionally high base set in H1 2025, the city still registered its third highest first-half leasing volume and the sixth-highest half-yearly performance since H1 2012. This underscores the continued depth of occupier demand and reinforces Chennai’s position as one of India’s most resilient office markets.

Supply activity gained significant momentum, with 2.6 mn sq ft of Grade A office space completed during the period—a 149% YoY increase. The sharp rise in completions reflects developers’ confidence in the market and their response to sustained demand rather than an oversupply scenario. This is evident from vacancy levels, which continued to decline to 8.5% despite the substantial addition of new stock, highlighting the market’s strong absorption capacity and healthy demand-supply balance.

With one of the lowest vacancy rates among major office markets in the country, Chennai continues to exhibit strong commercial real estate fundamentals, supported by resilient occupier demand, disciplined supply additions, and sustained developer confidence.

Residential Market Highlights of Chennai

Chennai’s residential market remained stable during H1 2026 despite Tamil Nadu state elections being round the corner, with housing sales growing by 3% YoY to 9,198 units, while launches dipped moderately by 0.3% YoY at 9,588 units. The market continued to be driven predominantly by genuine end-user demand, supported by the city’s diversified employment base, expanding infrastructure, and sustained economic activity.

The city’s housing market has increasingly transitioned towards mid and premium housing, reflecting evolving consumer aspirations for larger homes, better amenities, and lifestyle-oriented developments. Simultaneously, affordability pressures and rising construction costs have resulted in a declining share of affordable housing transactions.

CHENNAI RESIDENTIAL MARKET SUMMARY

| Parameter | H1 2026 | H1 2026 Change (YoY) |

| Launches (housing units) | 9,588 | -0.3% |

| Sales (housing units) | 9,198 | 3% |

| Average Price in INR/ sq ft | INR 7,555/sq ft | 5% |

Source: Knight Frank India Research

Demand shifts towards mid and premium housing

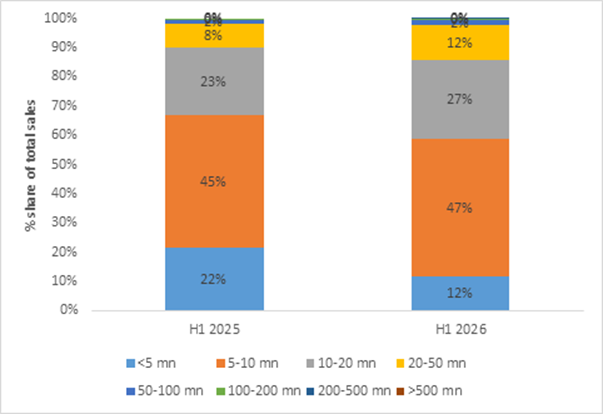

The Chennai residential market continued its structural shift towards higher-value housing during H1 2026.Homes priced between INR 5-10 mn remained the largest contributor to residential sales, accounting for 47% of total transactions. The INR 10-20 mn segment increased its share to 27%, while homes priced between INR 20-50 mn accounted for 12% of overall sales, reflecting rising buyer preference for larger homes, enhanced amenities and premium developments.

Conversely, the affordable housing segment priced below INR 5 mn witnessed its share decline sharply from 22% in H1 2025 to 12% in H1 2026, highlighting the impact of affordability pressures, rising input costs and constrained supply.

· Joseph Thilak, National Director – Occupier Strategy and Solutions (Hyderabad & Chennai), Knight Frank India, said “Chennai’s residential market continues to demonstrate remarkable resilience, supported by a diversified employment base, expanding infrastructure and sustained end-user demand. The steady growth in housing sales, alongside measured price appreciation, reflects the market’s healthy fundamentals. We are also witnessing a clear evolution in buyer preferences, with demand increasingly shifting towards mid and premium housing segments as consumers seek larger homes, better amenities and improved lifestyles. Looking ahead, continued investments in manufacturing, Global Capability Centres, metro connectivity and major infrastructure projects such as Chennai Metro Phase II and the proposed Parandur Airport are expected to further strengthen housing demand and reinforce Chennai’s position as one of India’s most stable residential markets.”

Balanced inventory levels reflect healthy market fundamentals

Despite an increase in unsold inventory to 19,722 units, Chennai’s residential market continues to remain fundamentally balanced. The city recorded an overall Quarters-to-Sell (QTS) of 4.4, indicating comfortable inventory levels supported by sustained end-user demand. The INR 5–10 mn segment remained one of the healthiest category with a QTS of 3.7, reflecting strong absorption. Meanwhile, inventory expanded across the mid and premium segments as developers responded to changing consumer preferences.

Residential prices continue to appreciate

Average residential prices in Chennai increased 5% YoY to INR 7,555 per sq ft, supported by sustained housing demand, expanding employment opportunities and continued infrastructure development across the city. Perambur registered the strongest appreciation with a 35% YoY increase bringing the average prices in the range of INR 10,563-11,158 sq ft per month, driven by infrastructure upgrades and enhanced metro connectivity. Perumbakkam recorded a 20% YoY rise owing to its proximity to the OMR employment corridor and upcoming Metro Phase II connectivity, while Mogappair witnessed 13% YoY appreciation, supported by strong end-user demand and established social infrastructure.

Office Market Highlights of Chennai

Chennai’s office market continued to demonstrate resilience in H1 2026, recording 3.6 mn sq ft of leasing activity. While transaction volumes fell by 28% YoY compared with the exceptionally strong H1 2025, leasing activity remained among the highest ever recorded for a first-half period, underscoring the city’s sustained appeal as a leading commercial real estate destination.

The city’s diversified economic base, competitive operating costs, deep talent pool and expanding infrastructure continued to attract a broad spectrum of occupiers across Global Capability Centres (GCCs), domestic enterprises, flex space operators and technology firms.

CHENNAI OFFICE MARKET SUMMARY

| Parameter | H1 2026 | H1 2026 Change (YoY) |

| Completions in mn sq ft | 2.6 mn sq ft | 149% |

| Transactions in mn sq ft | 3.6 mn sq ft | -28% |

| Average transacted rent in INR/sq ft/month | INR 74.5/sq ft/month | 7% |

Source: Knight Frank Research

End-User Categories

Global Capability Centres (GCCs) remained the largest occupier group in Chennai, accounting for 45% of total office leasing during H1 2026. While their share moderated slightly from the previous year, this reflected a broader diversification of the occupier base rather than weaker GCC demand. Large transactions by Citibank, Deloitte, and DHL reaffirmed Chennai’s appeal as a preferred hub for global operations.

Flexible workspace operators also expanded their footprint, accounting for 30% of total leasing, up from 20% a year earlier. Growth was driven by strong demand for managed offices and coworking spaces, with major transactions by WeWork, IndiQube, Simpliwork, and Workez highlighting the continued shift toward flexible workplace solutions.

Domestic occupiers emerged as a key growth driver, with leasing by India-facing businesses rising nearly 90% year-on-year and their share of total absorption increasing from 7% to 18%. Demand was led by the services sector, followed by BFSI, IT/ITeS, and manufacturing.

| End-User Licensee/Buyer | GCC | Flex | India-Facing Business | Third Party IT | Total |

| Area transacted in mn sq ft | 1.6 | 1.08 | 0.7 | 0.2 | 3.64 |

| % Share | 45% | 30% | 18% | 7% |

Source: Knight Frank Research

Joseph Thilak, National Director – Occupier Strategy and Solutions (Hyderabad & Chennai), Knight Frank India, said “Chennai’s office market continues to display exceptional resilience and depth. Although leasing activity moderated compared with the record levels witnessed last year, transaction volumes remain among the strongest ever recorded, highlighting the city’s enduring attractiveness to both domestic and global occupiers. We are seeing demand broaden beyond Global Capability Centres to include flexible office spaces and India-facing businesses, creating a more diversified and balanced occupier ecosystem. Combined with low vacancy levels, steady rental growth and significant infrastructure investments, Chennai remains well positioned to attract long-term commercial real estate investment while supporting future occupier expansion.”

Steady rental appreciation across business districts

Supported by healthy occupier demand and tight vacancy levels, Chennai recorded 7% YoY growth in average transacted office rentals, reaching INR 74.5 per sq ft per month. Among business districts, SBD OMR witnessed the strongest rental appreciation at 8% YoY, followed by SBD and PBD Ambattur, each recording 4% growth.

PBD OMR & GST Road registered 3% rental growth, while CBD recorded a modest 1% increase. The sustained rental appreciation across major office corridors reflects the city’s strengthening commercial fundamentals and continued demand for quality office assets.

BUSINESS DISTRICT-WISE RENTAL MOVEMENT

| Rental value range in H1 2026INR/sq ft/month | 12-month change | 6-month change | |

| CBD | 70-95 | 1% | 0% |

| SBD | 75-100 | 4% | 2% |

| SBD OMR | 80-125 | 8% | 3% |

| PBD OMR and GST Road | 58-75 | 3% | 2% |

| PBD Ambattur | 48-58 | 4% | 2% |

Source: Knight Frank Research